This is a financial promotion for The First Sentier China Strategy. This information is for professional clients only in the UK and EEA and elsewhere where lawful. Investing involves certain risks including:

- The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

- Currency risk: the Fund invests in assets which are denominated in other currencies; changes in exchange rates will affect the value of the Fund and could create losses. Currency control decisions made by governments could affect the value of the Fund's investments and could cause the Fund to defer or suspend redemptions of its shares.

- Single country / specific region risk: investing in a single country or specific region may be riskier than investing in a number of different countries or regions. Investing in a larger number of countries or regions helps spread risk.

- China market Risk: although China has seen rapid economic and structural development, investing there may still involve increased risks of political and governmental intervention, potentially limitations on the allocation of the Fund's capital, and legal, regulatory, economic and other risks including greater liquidity risk, restrictions on investment or transfer of assets, failed/delayed settlement and difficulties valuing securities..

- Concentration risk: the Fund invests in a relatively small number of companies which may be riskier than a fund that invests in a large number of companies.

- Smaller companies risk: Investments in smaller companies may be riskier and more difficult to buy and sell than investments in larger companies.

For details of the firms issuing this information and any funds referred to, please see Terms and Conditions and Important Information.

For a full description of the terms of investment and the risks please see the Prospectus and Key Investor Information Document for each Fund.

If you are in any doubt as to the suitability of our funds for your investment needs, please seek investment advice.

China Client Update - Can China claw back performance in the year of the tiger?

Once again, 2021 was a year full of surprises and challenges, with ongoing Covid disruptions and China turning from a global outperformer to underperformer. The Chinese government’s policy crackdowns, especially in the internet, education and property sectors, were sudden and dramatic. Meanwhile, inflation globally has moved from “transitory” to an ongoing threat to stability, coercing central banks like the US Federal Reserve to tighten from record levels of money supply, with its dampening effect being felt on correspondingly high stock prices.

Fed tightening will likely affect Hong Kong markets as well, given the city’s currency and interest rates linkage to the US. Over the past year, the Hang Seng Index has underperformed the Shanghai Composite by nearly 20 percentage points, mostly in the second half of 2021 as US inflation heated up, and the premium of A-shares over H-shares widened for large companies listed in both markets.

The year ahead also looks like a mixed picture – China is turning more accommodative in its policies but new Covid variants and persistent inflation remain key risks. The question on many investors’ minds is whether China can claw back its strong performance of previous years, which seems fitting as we enter the year of the tiger in the Chinese horoscope.

The Hang Seng underperformed the Shanghai Composite in 2021

Source: Factset, FSSA Investment Managers as of 31 December 2021.

As bottom-up investors, we have observed how companies navigated through the crises, such as by adopting new technologies, cutting excess costs or deploying their marketing or research and development (R&D) budgets more wisely. Broadly speaking, valuations have been falling to more reasonable levels, and we have taken opportunities to accumulate quality companies throughout the past year.

For example, companies related to the consumption-upgrade theme, including China Mengniu Dairy and ZTO Express, have been challenged, particularly as the Omicron variant outbreak prompted new lockdowns in some large cities. Recent data showed China’s retail sales grew by just 1.7% year-on-year in December, slowing from 3.9% in the prior month and missing expectations. We bought more of both companies on weakness – we are seeing competition in their respective industries ease, and their fundamentals remain solid.

We still believe that consumption upgrading will be a key growth driver for China over the next decade. Per capita consumption, from dairy to home appliances, insurance and sportswear, will structurally grow. In addition, preference for home-grown brands will continue to rise, helped not only by geopolitical tensions but also overseas travel restrictions. As usual, we look for companies with strong brands or other forms of competitive moats with long-term earnings visibility.

We recently bought ANTA Sports, China’s most successful sportswear company, and one of the few Chinese companies that has proven its ability to build and run multiple strong consumer brands. We believe it can significantly prolong its brand life-cycle and continue to grow sales, as it attracts new customers with its Kids, Fusion and performance sportswear range. Although the recent Covid lockdowns were a headwind on sales, our conviction was reinforced after a recent call with management which showed a healthy recovery trend in the fourth quarter of 2021.

Another recent portfolio addition is Xiaomi, a top 5 global smartphone brand with a growing network of partners within its Internet-of-Things (IoT) ecosystem, and rising contribution from internet services (mainly advertisements and gaming). We like the company mainly for its recurring business model – selling low-priced handsets and then monetising its internet services, thereby fostering high customer retention. In addition, the company has a clear and consistent strategy, strong execution, high alignment of interests and dedicated R&D staff.

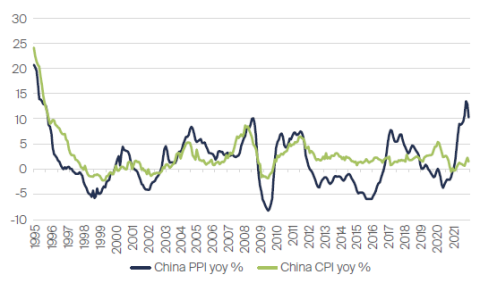

Ability to pass on inflation was a key differentiator

Unlike in the US where the consumer price index (CPI) has reached a multi-decade high of 7%, China’s inflation in the past year was mainly driven by constraints on the supply side. Last year the producer price index (PPI) rose to 13.5% in October, the highest level since 1995, but CPI peaked at only 2.3% the next month. Companies in Greater China were better positioned to cope if they had vertical integration, economies of scale, or simply sat more upstream in their supply chains.

China's recent inflation has been led by producers

Source: Bloomberg, FSSA Investment Managers, as of 20 January 2022.

For example, Taiwan Semiconductor (TSMC), the world’s largest chip-maker with more than 50% global market share, benefited from the semiconductor shortage, with solid sales growth and improved profitability. The company has increased capital expenditure and added capacity in response to strong customer demand. TSMC remains one of our top holdings in the Greater China region given its strong franchise and high standards for governance. It has generated attractive long-term shareholder returns with high levels of free cash flow, while its dividends per share has almost doubled over the last five years. It has also been a leader in sustainability efforts, with its focus on energy consumption and raw material efficiency.

On the other hand, Midea Group, China’s leading home appliances brand, performed less well last year as higher costs for raw materials and shipping put pressure on margins. In the longer term, we believe it should be able to pass through additional costs – either by increasing prices or by upgrading the product mix. It has also been streamlining its distribution channels and increasing the use of automation in the production process. We believe the core business can deliver around 10% earnings growth per year via moderate gains in selling prices, growing market share and margin expansion.

In the fourth quarter we initiated a position in Sinoseal, a China market leader in mechanical sealing equipment for large industrial customers, mostly petro-chemical producers and oil refineries. We are confident in Sinoseal’s ability to pass on inflationary pressures as mechanical seals have high barriers to entry, an oligopoly market structure, and a recurrent and sticky after-market. While mechanical seals are a crucial product for ensuring safety and output, the cost to the customer is quite low, and competition is limited. Sinoseal’s product quality is on par with multinationals (MNCs) and it has earned a strong reputation domestically, while enjoying a much lower cost base than foreign peers.

Exports reach new highs despite tensions with the US

From a political standpoint, we believe conflicts between China and the US will likely continue, whether that be on exports and trade or other geopolitical issues. We divested Hangzhou Hikvision after it was added to the US sanctions list. Additionally, we switched our positions in JD.com and ZTO Express from the American Depositary Receipts (ADRs) to the Hong Kong-listed shares, due to policy uncertainties in the Chinese ADR market.

That said, we believe the heated rhetoric between the US and China mainly affects market sentiment, rather than having a major impact on the economy. China’s economy is still very domestically driven and exports contribute only about a quarter to GDP growth.

What’s more, China’s export numbers continue to beat expectations and reach new highs. Before the pandemic, there were concerns that China might lose its manufacturing edge due to labour shortages. However, that concern is slowly diminishing. As global demand recovers, China has become a reliable manufacturing source for most markets around the world.

When the US-China trade war first started, Chinese exporters were sold off on fears of higher tariffs. However, looking at the exporter companies in our portfolio today, profit levels have been broadly unaffected despite the introduction of tariffs and many continue to enjoy growing overseas sales.

Techtronic, one of the world’s largest producers of branded power tools, is an example of a stalwart exporter in our portfolio, with about 75% of its revenue coming from North America and another 15% from Europe. Founded in the mid-1980s and listed in Hong Kong in 1991, Techtronic now occupies a leading position in North America (around 24% market share by retail value of power tools) with key brands such as Milwaukee, AEG and Ryobi. Techtronic spends significantly on R&D to improve existing products and create new categories, which has helped to boost margins. They were also the first to move towards cordless products (which eventually shaped the entire industry).

The stock performed well last year as it reported better-than-expected earnings. The company’s sales growth outlook also looks rosy, as it should benefit from the proposed USD 2trn infrastructure bill in the US. In the past, its manufacturing base was only in China, but it is now developing in Southeast Asia — Vietnam, in particular — and also looking to expand in the US.

Smaller niche companies have also benefited from robust overseas demand. We recently purchased Shenzhen Mindray Bio-Medical Electronics, China’s largest domestic medical devices company and a market leader in patient monitors and life support systems. The company has a strong track record and has been gaining market share from global leaders as it expands its presence overseas. During 2015-20, sales to overseas markets grew at a compound annual rate of 31%, faster than the 25% for China sales which we also find attractive. We believe there are significant opportunities ahead, as the penetration level of medical devices in China is still low and there is a growing preference for import substitutions.

Chinese regulators treading lightly around systemic risk

In the A-share market, we expect a gradual normalising after the pandemic-related events of the last two years. Unlike the US, Europe and Japan, China had been tightening for several years, which means the People’s Bank of China has more room to ease to prop up the economy. Things came to a head last year as the “three red lines” policy1 caused overleveraged property developers like Evergrande to default on bonds and halt certain developments.

In setting monetary policy, China will need to balance its goal of tempering supply-side inflation with a slowing economy, ageing population, and weak sentiment in the property sector. Policymakers started to reverse some policies once the risks of contagion appeared too big to ignore. The recent cuts to the reserve requirement ratio (RRR) and loan prime rate (LPR) signalled that Beijing is willing to add some cushioning. As rates start to tighten elsewhere, China may look more attractive to global investors as the government turns more pro-growth.

We expect further policy actions to come but the government will remain prudent and fine-tuned, as the goal is stability. Recently media reports said that policymakers plan to relax the three red lines policy by excluding debt accrued from acquiring distressed assets, which should encourage industry consolidation.

We believe China Resources Land (CR Land) is well positioned to benefit from such consolidation with its healthy balance sheet and strong portfolio of investments. Recent policy constraints have hurt profits at the more leveraged players, but conversely should provide a boost to less leveraged companies like CR Land.

One of the company’s key strengths is its ability to acquire land through projects, which can be higher margin compared to land-bidding auctions. Additionally, its deep-rooted connections in Shenzhen and its reputation in investment property operations is a major advantage when competing for urban renewable projects and transit-oriented development projects. Revenue grew at 64% in 1H2021 with solid 31% gross margins, while net gearing declined.

While we have limited exposure to property companies, we own a number of holdings which should benefit from home upgrades. In our A-share portfolio, Zhejiang Weixing New Building Materials, a leading household drain pipe company, performed well over the year despite a pullback in the third quarter when it was challenged by rising raw material prices. There was strong growth in the retail market and the pressures from higher raw material costs have abated somewhat, with recent price hikes feeding into the company’s bottom line. Government signals on the easing of real estate market restrictions also helped its performance.

The company’s culture seems prudent about business development, an important trait in these volatile times for the property sector. On a recent call with the company, Chairman Jin Hongyang said, “Similar to the human body, the most important thing for operating a business is to maintain the health.” As such, we believe the company will not be too aggressive to generate growth and acquire other businesses. This aligns well with our focus on investing in companies with quality and sustainable growth. Overall, we believe Zhejiang Weixing can achieve 10-15% earnings growth per annum through to 2025.

The robust performance of Zhejiang Weixing prompted a closer look at the sector, and we added peer company Beijing New Building Materials, the largest gypsum board company in China, to our A-share portfolio. The company has a strong franchise, with limited competition, resilient demand and more than 60% market share in both high-end and mass markets. Gypsum board is a good, low-cost building material and is lightweight, fireproof and a heat insulator. Consumption in China is low at 2.5 square metres (sqm) per capita, compared to the US (7 sqm), Europe (6 sqm) and Japan (4 sqm), which implies plenty of room to grow. The company also plans to build new capacity in overseas markets, and recently acquired a few companies to expand into the waterproofing business.

Observations and outlook

China is dealing with many of the same problems as other countries around the world – widening wealth gaps, an ageing population with low birth rates, and climate change (covered in our recent update on China’s net zero drive). The recent reforms are not run-of-the-mill and will likely have lasting consequences. Meanwhile the Chinese economy may continue slowing on a structural basis, even as the population’s wealth rises. Despite this, China is still a relatively poor country (USD 10-11k per capita income) and there remains plenty of runway for growth, even with a compromised outlook.

We ground our observations in what we see and hear from companies, on a bottom-up basis. The scale of the property market is unsustainable, while the investment-driven nature of the economy is already leading to materially lower capital-productivity, lower growth and lower returns.

Some of China’s reforms are a rational response to these observations. While the Chinese economy is three-quarters the size of the US, the property market is twice the size, which shows how far things are out of balance. Most economists believe that property accounts for as much as 25-30% of GDP, which is two-to-three times bigger than most countries, while around the world, property (in this era of free-money) is generally regarded as being at historically high and unsustainable levels.

The newspapers have been replete with stories about ghost cities in China – empty apartments and 1.5 apartments per citizen – for the last decade. In that sense, the property market bubble has been called many times over the years, but there is now a sense that political will and economic development have collided, and there will finally be change.

More specifically, property accounts for around 80% of Chinese household wealth, which compares with the likes of Tokyo at 65% in 1989. The analogy should not be overdone, but Japan’s bubble has been deflating ever since (though Japan had already succeeded in becoming a rich, stable and developed country). The other similarity would be in demographics, with some making the observation that China will not succeed in becoming rich before it gets old (unlike Japan). All of this means that property-affordability is very low and debt levels are clearly high in China. Evergrande is but one part of this, with more than USD 300bn of debt.

On the other hand, we do not anticipate a Lehman-style bust, with the economy still mostly closed and the authorities able to provide liquidity, as well as direct the banks and other property companies to provide a solution. Absorption of these excesses will clearly take time and the most likely outcome is slower growth. In our view, irrespective of the policy risks, this should mean lower valuation multiples.

Meanwhile, efforts to rebalance the economy from investment (property and infrastructure) to consumption will likely prove challenging because it requires higher wages, which would undermine export growth. And it is imperative, for political and stability reasons, that the property market doesn’t break. Muddling through would be a good outcome and per China’s historical economic development seems quite likely.

“Common Prosperity” is the new name for this rebalancing and is part of the solution, with forcible redistribution from the internet companies, closure of the private tutoring industry, large “fines” and even larger “donations” across a range of businesses. This will help, but seems unlikely to lead to a significant shift in the near term. Meanwhile it is clearly negative for returns and growth, particularly in the private sector.

In such an environment, we strive to be careful, and to concentrate on persistency of returns and capital preservation with reasonable growth. As such, we continue to adhere to our long-established investment philosophy and process, with our broad exposure to the Greater China region including fabulous companies in Hong Kong and Taiwan as well as mainland China.

1 Outlined by the central government in August 2020, the three red lines define limits on borrowings. They are: a liability-to-asset ratio excluding advance receipts of less than 70%; a net debt-to-equity ratio of less than 100%; and a cash to short-term debt ratio of one.

Related insights

Source: Company data retrieved from company annual reports or other such investor reports. Financial metrics and valuations are from FactSet and Bloomberg. As at 31 December 2021 or otherwise noted.

Important information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should conduct your own due diligence and consider your individual investment needs, objectives and financial situation and read the relevant offering documents for details including the risk factors disclosure. Any person who acts upon, or changes their investment position in reliance on, the information contained in these materials does so entirely at their own risk.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication but the information contained in the material may be subject to change thereafter without notice. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

Past performance is not indicative of future performance. All investment involves risks and the value of investments and the income from them may go down as well as up and you may not get back your original investment. Actual outcomes or results may differ materially from those discussed. Readers must not place undue reliance on forward-looking statements as there is no certainty that conditions current at the time of publication will continue.

References to specific securities (if any) are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. Any securities referenced may or may not form part of the holdings of First Sentier Investors' portfolios at a certain point in time, and the holdings may change over time.

References to comparative benchmarks or indices (if any) are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from the funds managed by First Sentier Investors.

Selling restrictions

Not all First Sentier Investors products are available in all jurisdictions.

This material is neither directed at nor intended to be accessed by persons resident in, or citizens of any country, or types or categories of individual where to allow such access would be unlawful or where it would require any registration, filing, application for any licence or approval or other steps to be taken by First Sentier Investors in order to comply with local laws or regulatory requirements in such country.

This material is intended for ‘professional clients’ (as defined by the UK Financial Conduct Authority, or under MiFID II), ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) or Financial Markets Conduct Act 2013 (New Zealand) and ‘professional’ and ‘institutional’ investors as may be defined in the jurisdiction in which the material is received, including Hong Kong, Singapore and the United States, and should not be relied upon by or be passed to other persons.

The First Sentier Investors funds referenced in these materials are not registered for sale in the United States and this document is not an offer for sale of funds to US persons (as such term is used in Regulation S promulgated under the 1933 Act). Fund-specific information has been provided to illustrate First Sentier Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group (MUFG). Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors and Realindex Investments, all of which are part of the First Sentier Investors group.

This material may not be copied or reproduced in whole or in part, and in any form or by any means circulated without the prior written consent of First Sentier Investors.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:[1]

· Australia and New Zealand by First Sentier Investors (Australia) IM Limited, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

· European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

· Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong

· Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) is a business division of First Sentier Investors (Singapore).

· Japan by First Sentier Investors (Japan) Limited, authorised and regulated by the Financial Service Agency (Director of Kanto Local Finance Bureau (Registered Financial Institutions) No.2611)

· United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

· United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167).

· Other jurisdictions, where this document may lawfully be issued, by First Sentier Investors International IM Limited, authorised and regulated in the UK by the Financial Conduct Authority (registration number 122512; registered office 23 St. Andrew Square, Edinburgh, EH2 1BB number SC079063).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group

1 If the materials will be made available in other locations, seek advice from Regulatory Compliance.