India’s economic resurgence amidst the turbulence

What are your thoughts on the high valuations in India?

Vinay: Over the last few years, we have been selling many companies which have become expensive. On the other hand, there are still companies that are attractively valued with robust growth ahead. Our portfolio has an average return on capital employed (ROCE) of over 30% and trades on 20x earnings, which should grow around 15% per year on average.

For example, we had been shareholders in two IT consulting companies for a long time when Covid hit in 2020. In 2021, when it looked like everything would go digital, revenue visibility for these companies increased and the market extrapolated from it. These companies saved on costs as people stopped travelling, so their margins expanded. Their valuations rose from 15x earnings to 30x - 40x last year.

We were less optimistic, and thought that growth and margins would fall, along with valuations, so we sold most of our holdings last year. This year, as these concerns have come to the fore and investors reduced their forecasts, their valuations have become more reasonable and we have started buying again. However, we think the concerns have not played out yet, so we will wait for a better opportunity to buy more.

How are you different from other asset managers?

Vinay: Firstly, when we invest in companies, we are very clear about what we will not do. It is easy to exclude certain practices like tobacco, weapons, gambling, and modern slavery. What is more difficult is assessing who are the people we will not back. For example, we have never invested in two of the largest business groups in India, because of the way they were built and managed, and how they influenced policymaking to their advantage. We will never own them, regardless of how attractive they become in terms of growth or valuations.

The second thing we do differently is that we focus on the people and culture of the businesses we are interested in. We don’t build sophisticated spreadsheets in which we try to predict a company’s future. Instead, we look at how a company started, who started it, and how it evolved over the cycles — has it been fair to all stakeholders, and what kind of capital allocation decisions were made. We consider how they think about minority shareholders and other stakeholders, and what kind of governance structures they are building. We pay attention to what the board looks like, is there enough independence, is it effective, and whether the family wants it to be effective.

We also pay attention to how the managers are incentivised, their key performance indicators (KPIs), and whether we are aligned over the long term. At many companies, the managers are only incentivised according to revenue or earnings growth. This often comes with acquisitions, increasing leverage and decreasing returns on capital. We think effective KPIs should result in higher return on capital employed (ROCE), and we engage with our companies on this.

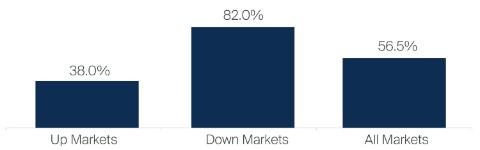

The third aspect which sets us apart is our focus on capital preservation. We have an absolute return mindset and think of risk in terms of losing money rather than underperforming a benchmark. In our team discussions, we think about the many things that can go wrong. Since inception through September 2022, we outperformed the market 38% of the time when markets were up, but in down-markets we performed better around 82% of the time. This preserved capital and created value for our investors over the long term.

Our investment style is inherently conservative

These figures refer to the past. Past performance is not a reliable indicator of future results. For investors based in countries with currencies other than USD, the return may increase or decrease as a result of currency fluctuations. All performance data for the FSSA Indian Subcontinent composite in USD. Source: First Sentier Investors. Source for benchmark — MSCI. Months of outperformance vs benchmark (MSCI India Index) since inception December 31, 2002. Performance data is calculated in USD on a net of fees basis and includes income reinvested net of withholding tax. This information is provided for illustrative purposes to demonstrate FSSA's activity within the strategy for the period shown.

Observing leadership changes at an Indian biscuit company

Vinay: The following examples may help to illustrate the above points. First is an Indian biscuit company, where we have been shareholders for a long time. We have met this company regularly over the last 20 years, paying attention to the changes in management and whether the governance structures were adequate to protect minority shareholders.

The company was established in 1892 and the promoter family became shareholders in the early 1990s. The family also owns companies in areas like property and airlines — such businesses often require cash and we were concerned that the biscuit company may have to fund the struggling parts of the group. We also worried about whether the next generation of the family would return to run the business (usually a negative indicator). When we first looked at the biscuit company, we thought the board could be stronger.

In 1993, the company’s first professional CEO was appointed and the business became very successful. However, he was fired in 2003 and there was no new CEO until 2005. The company’s biggest competitor started gaining market share, while a new competitor also launched around this time. At this point, we bought shares as valuations had become attractive at under 1x price-to-sales.

Another CEO subsequently joined in 2005, bringing deep experience. When the third professional CEO took over in 2013, he changed the business mix towards more premium products and increased margins.

After all of this and despite changing hands several times, the franchise was still very strong in terms of the brands that the company owned. We thought that the industry was attractive and underpenetrated, and the company could earn decent returns on capital.

We have continued to meet with the company over the years to engage with the management on key issues. As long-term shareholders, we have put forward our views on its share incentive schemes, board independence and intercorporate deposits (among other topics). The company has since improved in all of these areas.

Improving culture and governance at a telecom company

Sree: A second example is an Indian telecom company. We have known the company since the early 2000s and met the management more than 40 times over this period. We saw it become dominant in the domestic market as telecom penetration increased. Throughout this period, we had a number of concerns around the governance as well as the risk appetite of the founder.

This came to the fore when the company acquired a large telco in Africa. In a magazine interview at that time, the founder said, “I am like a junkie looking for his next fix.” This was clearly a culture that we would not back.

However, we began to see signs of change around 2016. A new entrant was disrupting India’s telecom industry. The company’s promoters realised that the only way to survive was to make significant changes, including to the governance and culture of the company.

A professional CEO was hired and he brought in the governance standards of a multinational company (MNC). In addition, there was a public admission by the founder that the investment in Africa was a mistake. This showed his increasing humility and changing approach in terms of risk appetite and capital allocation. The group subsequently exited a number of unprofitable markets and spun off the Africa subsidiary.

Meanwhile, a leading telecom provider in Singapore had become the largest shareholder, with a stake bigger than that of the founding family. We met the CEO of that company, who played an increasing role in building guardrails around capital allocation and governance.

As we saw the company change for the better with many of our concerns alleviated, we initiated a position in 2017. In the following years, the company benefited from industry consolidation as the disruption from the new entrant waned. The company also became more efficient and improved its capital allocation. It is now one of the largest positions in our portfolio.

Engaging on capital allocation discipline at an automotive manufacturer

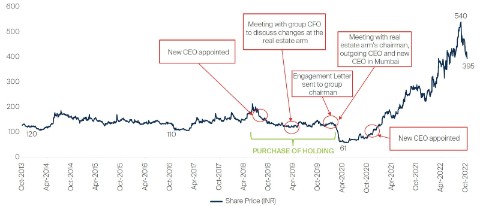

Sree: A third example began as an automotive manufacturer and grew into a large conglomerate. We have known the company for decades and always held them in high regard for their governance standards. Despite this, we were not shareholders for most of the last seven years because we thought the group’s capital allocation discipline was deteriorating. At one point it had over 150 subsidiaries, many of which were loss-making and too complicated for us to understand.

We were also shareholders of the real estate arm of the group. This company should have benefited from the shift in demand towards larger, well-reputed developers. But due to internal issues, the company failed to capitalise on these opportunities, which disappointed shareholders.

In 2020 we wrote a letter to the group chairman, highlighting our concerns around the capital allocation of the group and the poor performance of the real estate arm. We received a prompt reply in which he acknowledged our concerns and mentioned that the group is setting up a new capital allocation framework. He referred us to the deputy CEO who was set to take over as group CEO and was driving this change.

When we met the new group CEO earlier this year, we saw significant changes taking place in the company’s capital allocation. The group had exited or sold many of their lossmaking businesses. More importantly, he announced that the group would exit or sell any subsidiary which did not meet the return on equity (ROE) threshold of 18% within a certain timeframe. We had seen similar changes at other companies and the great results that had brought for shareholders. We became shareholders earlier this year.

Meanwhile, at the real estate arm, he was making the necessary changes for it to reach its potential. Over the last few years, there have been two new CEOs — the first one didn’t work out, but the second CEO was an outsider to the business who then replaced a majority of the senior management team. There has been a significant improvement in the company’s growth profile and profitability since then.

These examples show that if there is a management change which brings more discipline around capital allocation or governance, a re-rating tends to happen.

Indian conglomerate's real estate arm

Source: FSSA Investment Managers, Bloomberg, October 2022.

What is worrying the team at this time?

Vinay: In the medium to long term, the creation of enough job opportunities is a key concern. India’s economy has a disproportionately high share in the services sector, and manufacturing needs to expand to raise employment. Otherwise we risk having more social inequality, as India has a young population, many of whom are poor.

Another concern is the increasing concentration of corporate heft. There are two groups in India which seem like they will end up owning everything in India. If that happens, the country will become an oligarchy, which could be a longer-term risk for valuations.

I also worry about the bubble forming in high-quality companies when they decide to enter new categories, as investors tend to reward them with higher valuations based on lofty expectations. This could be an auto component maker wanting to expand into electric cars and car batteries, and trading on 70x price-to-earnings. Or when a pipe manufacturer decides to make paints and adhesives, and starts trading on similar valuations as Asian Paints. One needs to be careful of such businesses.

Sree: Another worry is that in the past, many countries have grown by depleting resources. While India has a lot of growth potential, it has to become more sustainable. For example, we expect car ownership to increase as income levels rise, but many of the most polluted cities in the world are in India. Therefore, companies and the government have to work together towards more sustainable growth.

How far along are Indian companies on the path to sustainability?

Vinay: We do not think there is such thing as a perfect company, there are only shades of grey. We try to help our companies to travel in the right direction. Meanwhile we are also learning and growing in this regard. We have always thought that if a company gets the governance right, and the owners and management care about all of their stakeholders, then even if they are behind on environmental and social factors, they will learn and improve over time. On the other hand, if the governance is lacking, then a company is just greenwashing and making noise.

Sree: We own one cement company and have engaged with them on worker safety. Their safety track record is far superior compared to peers — the CEO said that a plant manager’s incentivisation is affected by even a single injury in the plant, which holds their people accountable. Additionally, the company’s carbon footprint is about 10% lower than its peers in India. When we introduced them to a company that develops carbon capture technologies, that discussion was taken forward by the CEO. We were pleasantly surprised by their willingness to engage, learn and improve.

What excites you about India in the coming 10 to 20 years?

Vinay: I have been investing in India for the last 20 years. Consumer habits are changing, which is quite exciting. For example, in the early years, there was a case for increasing penetration in basic consumer staples like soaps, shampoos and laundry detergents. Today many of these categories are well penetrated and a higher share of consumer budgets are moving towards discretionary products. Indians are buying new vehicles and homes and everything that goes with it, like pipes or construction chemicals.

Similarly for financial businesses, the industry was underpenetrated 20 years ago. The incumbent state-owned banks were dominant with over 80% market share. Well-run private banks gradually gained market share and state-owned banks’ share fell to 60%. As basic deposit accounts have become more common, in the coming 10 to 20 years we expect more demand for insurance and wealth management products. We own companies which should benefit from this, such as a registrar and transfer agent (RTA) for mutual fund companies, and a general insurance business.

Sree: We are also excited by the large opportunity set of businesses that are small but will become large over time. An example is one of the leading domestic air conditioner companies. This is a high-quality, well-governed company with high returns on capital. India has an air conditioner penetration rate of 5% and there are a few million units sold each year. This compares with several tens of millions of ACs sold in other markets in the region, where penetration can reach 70%. We think this business could become several times its current size. It is a large business of the future, hiding in a small market capitalization currently.

Investment insights

- Article

- 3 mins

- Article

- 4 mins

- Article

- 3 mins

Company data retrieved from company annual reports or other such investor reports. Financial metrics and valuations are from FactSet and Bloomberg. As at 31 October 2022 or otherwise noted.

Important Information

This material is solely for the attention of institutional, professional, qualified or sophisticated investors and distributors who qualify as qualified purchasers under the Investment Company Act of 1940 and as accredited investors under Rule 501 of SEC Regulation D under the US Securities Act of 1933 (“1933 Act”). It is not to be distributed to the general public, private customers or retail investors in any jurisdiction whatsoever.

This presentation is issued by First Sentier Investors (US) LLC (“FSI”), a member of Mitsubishi UFJ Financial Group, Inc., a global financial group. The information included within this presentation is furnished on a confidential basis and should not be copied, reproduced or redistributed without the prior written consent of FSI or any of its affiliates. This document is not an offer for sale of funds to US persons (as such term is used in Regulation S promulgated under the 1933 Act). Fund-specific information has been provided to illustrate First Sentier Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results. This material is provided for information purposes only and does not constitute a recommendation, a solicitation, an offer, an advice or an invitation to purchase or sell any fund and should in no case be interpreted as such.

Any investment with FSI should form part of a diversified portfolio and be considered a long term investment. Prospective investors should be aware that returns over the short term may not be indicative of potential long term returns. Investors should always seek independent financial advice before making any investment decision. The value of an investment and any income from it may go down as well as up. An investor may not get back the amount invested and past performance information is not a guide to future performance, which is not guaranteed.

Certain statements, estimates, and projections in this document may be forward-looking statements. These forwardlooking statements are based upon First Sentier Investors’ current assumptions and beliefs, in light of currently available information, but involve known and unknown risks and uncertainties. Actual actions or results may differ materially from those discussed. Actual returns can be affected by many factors, including, but not limited to, inaccurate assumptions, known or unknown risks and uncertainties and other factors that may cause actual results, performance, or achievements to be materially different. Readers are cautioned not to place undue reliance on these forward-looking statements. There is no certainty that current conditions will last, and First Sentier Investors undertakes no obligation to publicly update any forward-looking statement.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE PERFORMANCE.

Reference to the names of each company mentioned in this communication is merely for explaining the investment strategy, and should not be construed as investment advice or investment recommendation of those companies. Companies mentioned herein may or may not form part of the holdings of FSI.

For more information please visit www.firstsentierinvestors.com. Telephone calls with FSI may be recorded.