Positioning for resilience in volatile times

FSSA Investment Managers has been investing in Asia and global emerging markets for three decades. We are conservative investors, and resilience during market sell-offs has underpinned our long-term performance. We believe this is an outcome of our unrelenting focus on quality.

As bottom-up stock pickers, we focus on company fundamentals, such as the competitive moat and the management. Even good companies are tested in downturns, but the qualities they exhibit often lead to greater advantages when the external environment improves. Investing in quality companies gives us the conviction to add to a position when the price has fallen.

The following are some of the factors we seek when selecting companies to invest in.

Before the storm

Long-term earnings growth and structural tailwinds

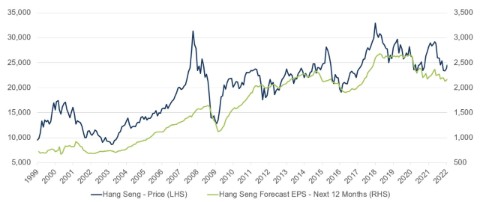

Clients often ask us about the macro environment and whether it will be a V-shape, L-shape or U-shape recovery, or if there will be a hard or soft landing. The honest answer is that we don’t know – none of us can predict the future. In our experience, company earnings drive share prices. So while property cycles and economic cycles are important, we believe a better question to ask is, “What will happen to company earnings in the next five to ten years?” As the share price is likely to follow.

Stocks tend to follow earnings in the long run

Hang Seng Index Price vs. 12-month EPS Forecasts

Source: Factset, FSSA Investment Managers, February 2022.

Part of this is finding long-term structural growth drivers to support our bottom-up company research. For example, China’s ageing population and shrinking workforce means that automation should be a growing trend. Last year was a record-low year for birth rates in China. Based on the demographic trend, in the next 10 or 20 years there should be increasing demand for robotic equipment as well as components that can improve the production process.

Meanwhile, healthcare spending in China is much lower than in developed countries. This, combined with China’s ageing population means that demand for healthcare should remain steady, despite the short-term policy noise. Other trends driving growth in the healthcare sector include domestic companies moving up the innovation curve and consolidation among the industry leaders.

The people factor

The FSSA team spends a significant amount of time assessing the people leading a company. We particularly like to see leaders that are risk aware and humble, like Sandeep Bakhshi, CEO of ICICI Bank, or those that look after a broader set of stakeholders, like Joey Wat, CEO of Yum China, which has one of the most generous employee benefit programs in China. Or managers that constantly try to be forward-looking, like MercodoLibre’s CFO Pedro Arnt, who is known for his lack of complacency.

The next thing we look for is alignment of interests. We want to see simple corporate structures and long-term-minded owners who are on the same page as minority shareholders. We do not like to see complicated structures, cross holdings, dual share classes which benefit one set of owners versus the others, or companies that have state ownership, as their interests may be different from ours. We tend to shy away from IPOs due to the asymmetric risk between the sellers and the new shareholders.

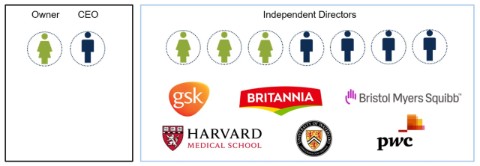

We also focus on boards and their composition. They are the ones responsible for business strategy, capital allocation, and incentive structures. Therefore, it is important for a board to be comprised mostly of independent directors who have the experience of serving in other organisations and are likely to stand up for minority shareholders when things go wrong. A good example among our holdings is Syngene International, a biotech manufacturing company in India. The board is majority independent with only the owner and the CEO on the board as insiders. The rest of the directors come from a tapestry of reputable organisations.

Company example: Syngene International (India)

Source: Company reports or website syngeneintl.com, as at March 2022.

This focus on governance has helped us avoid some pitfalls. For example, we had no investments in Russia prior to the invasion of Ukraine. We have always found it hard to invest in Russia given our focus on governance and quality. Whenever we carried out due diligence on a company, its ownership would include someone who would be close to Putin. This was a difficult roadblock for us to overcome. As a result, we have not had to make any changes to the portfolio amid the recent global tensions with Russia.

Dominant industry positions with strong competitive advantages

While governance is paramount, we also look for strong business models with solid long-term growth prospects. We tend to focus on companies that benefit from domestic demand and have circular long-term growth drivers such as demographics, urbanisation, productivity catch-ups, or import substitution. These companies may operate in smaller industries, but from experience and observing other economies, we know that these industries tend to become larger as incomes grow.

Additionally, each of our holdings should have a clearly defined competitive advantage. For example, airports are a legal monopoly – they are retail businesses with captive consumers that tend to come from the higher income segments of society. Another example of a competitive advantage is economies of scale, like with JD.com. As they grow in scale, these companies can give back those advantages to consumers and set up a virtuous, enduring cycle of growth. A trusted brand name such as Colgate-Palmolive, or quick-service restaurants like Domino's can also be considered a competitive advantage. They have significant moats in terms of what they represent to customers and the premium they can therefore charge. This helps to protect margins during challenging periods.

Another sign of a sustainable competitive advantage is high cash generation. We dislike companies that need large amounts of capital to grow cash flows. We focus on asset intensity, working capital, and free cash flow generation as metrics.

Putting all this together, we look for businesses with good governance, strong competitive advantages and solid prospects; in other words, companies that can sustainably compound cash flows at high rates.

During a crisis

When the market falls, we typically do not turn over our portfolios or sell out of our existing holdings. There is a strong belief on our team that every crisis presents an opportunity. During weak markets, better-quality companies often have an opportunity to gain market share and become stronger – and we can buy them at more reasonable prices than before. That said, when a market shock such as a pandemic or geopolitical conflict occurs, we may conduct additional checks on our assumptions and revisit our target valuations and conviction levels.

Some of the additional factors we check include:

Business performance (e.g. sales/margins) during previous downturns

If a company has shown resilience in a previous downturn, that can bode well for the current situation. We own Recruit Holdings in Japan, which is a leader in the global human resources (HR) industry. Recruit’s main growth driver is its HR technology business, primarily through Indeed, the largest online career search engine in the world.

The business demonstrated its resilience through the Covid recessionary period, as revenue was virtually flat in fiscal year (FY) 2021, while margins declined only slightly. Driven by labour shortages and strong pent-up demand, revenue subsequently more than doubled in the first half of FY2022 and margins surged. As market sentiment turned this January, Recruit was sold off on concerns that its high growth would be unsustainable, though the number of job postings continues to trend strongly across the US, Europe and Australia. We are confident that the company will recover, given its sound fundamentals.

How management teams have responded to the Covid pandemic

We were challenged in the early stages of the pandemic, given the unprecedented lockdowns and uncertainty. What ultimately gave us confidence were the meetings we held with management in that period. We realised that while the crisis was negative, many of our holdings would end up benefiting in the long run relative to their competitors.

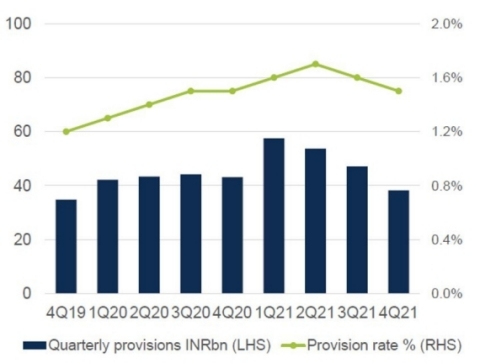

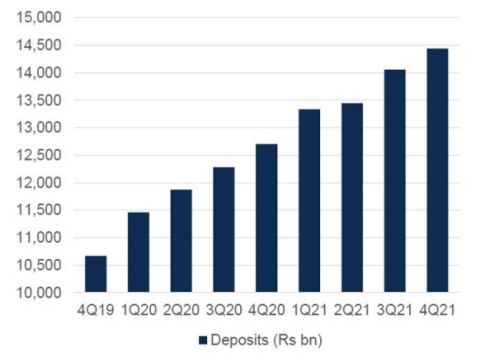

One example is HDFC Bank in India. At the height of the pandemic, as India came to a standstill for four months, HDFC Bank's customers had zero revenues and there were serious questions about how they would pay their interest costs. However, HDFC Bank’s actual provision rates did not rise much during that period, while deposits accelerated significantly. In our view, that is another feature of well-managed and reputable banks. During periods of stress, there is a flight to safety and depositors move their savings to banks that they believe are better placed.

Provisioning was relatively steady...

...while deposit growth accelerated

Source: Company materials, FSSA Investment Managers. Data as at 31 December 2021.

In fact, this is typical of all the banks we have invested in across other markets within our strategy: they generally have industry-leading deposit franchises, which gives them a cost of funds advantage during tough times. They have risk-aware and countercyclically-minded management teams, and they usually come out of crises with higher market share, better returns and an improved customer base.

We have been invested in HDFC Bank for nearly two decades and we saw these advantages come to the fore during the global financial crisis (GFC) in 2008, the taper tantrum in 2013 and again during the lockdowns over the last one and a half years in India. With our views on the quality of HDFC Bank – and having spoken with the CEO – we concluded that it should emerge from the pandemic stronger than ever.

What we focus less on

Commodity prices, interest rates, and other major macro factors

As bottom-up investors, we cannot forecast macro movements or outsmart the market on a short-term basis, but we are resolute in our belief that quality always pays off in the end. If we invest on at least a 3-5 year time horizon and seek out capable companies that are focused on long-term and sustainable growth, we believe we can continue to deliver reasonable absolute returns for our clients.

Unsustainable earnings growth

In our view, not all earnings should be judged similarly – earnings that are mostly delivered in cash and from highly recurring revenue or new avenues of growth are more sustainable. Less sustainable are those earned in a cyclical recovery, or from reflationary trends, leverage, share buybacks, or requiring a greater amount of capital.

Market volatility and short-term relative weakness

We are convinced that the way to achieve superior long-term returns is to focus on long-term absolute returns. By being benchmark agnostic, we can position our portfolios differently from the crowd, during times of widespread fear as well as euphoria. Amid the recent market weakness, we have taken advantage of the lower valuations to add to existing holdings and those ranked as high quality on our watch-list.

Building conviction in individual companies

We are experiencing volatile times, with interest rate hikes led by the US Federal Reserve, the Russia-Ukraine conflict, trade and technology tensions between China and the US, and China’s Covid resurgence and regulatory crackdowns being just a few of the latest flashpoints. By listing out the key components of quality, we hope to shed light on how we maintain our investment discipline and adhere to our long-standing investment philosophy and process, which we believe is the most important thing to do during uncertain times. To us, short-term market volatility is not a reason to pull back our risk appetite, but rather an opportunity to add high-quality companies at more attractive valuations.

We cannot predict the nature or severity of the next downturn. Nor can we expect positive performance in all market conditions. But we are assured that, after experiencing many cycles over the past three decades, our investment process has proven its resilience over the long term.

Note: Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time.

Important information

This material is for general information purposes only. It does not constitute investment or financial advice and does not take into account any specific investment objectives, financial situation or needs. This is not an offer to provide asset management services, is not a recommendation or an offer or solicitation to buy, hold or sell any security or to execute any agreement for portfolio management or investment advisory services and this material has not been prepared in connection with any such offer. Before making any investment decision you should conduct your own due diligence and consider your individual investment needs, objectives and financial situation and read the relevant offering documents for details including the risk factors disclosure. Any person who acts upon, or changes their investment position in reliance on, the information contained in these materials does so entirely at their own risk.

We have taken reasonable care to ensure that this material is accurate, current, and complete and fit for its intended purpose and audience as at the date of publication but the information contained in the material may be subject to change thereafter without notice. No assurance is given or liability accepted regarding the accuracy, validity or completeness of this material.

To the extent this material contains any expression of opinion or forward-looking statements, such opinions and statements are based on assumptions, matters and sources believed to be true and reliable at the time of publication only. This material reflects the views of the individual writers only. Those views may change, may not prove to be valid and may not reflect the views of everyone at First Sentier Investors.

Past performance is not indicative of future performance. All investment involves risks and the value of investments and the income from them may go down as well as up and you may not get back your original investment. Actual outcomes or results may differ materially from those discussed. Readers must not place undue reliance on forward-looking statements as there is no certainty that conditions current at the time of publication will continue.

References to specific securities (if any) are included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. Any securities referenced may or may not form part of the holdings of First Sentier Investors' portfolios at a certain point in time, and the holdings may change over time.

References to comparative benchmarks or indices (if any) are for illustrative and comparison purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, and have limitations when used for comparison or other purposes because they may have volatility, credit, or other material characteristics (such as number and types of securities) that are different from the funds managed by First Sentier Investors.

Selling restrictions

Not all First Sentier Investors products are available in all jurisdictions.

This material is neither directed at nor intended to be accessed by persons resident in, or citizens of any country, or types or categories of individual where to allow such access would be unlawful or where it would require any registration, filing, application for any licence or approval or other steps to be taken by First Sentier Investors in order to comply with local laws or regulatory requirements in such country.

This material is intended for ‘professional clients’ (as defined by the UK Financial Conduct Authority, or under MiFID II), ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) or Financial Markets Conduct Act 2013 (New Zealand) and ‘professional’ and ‘institutional’ investors as may be defined in the jurisdiction in which the material is received, including Hong Kong, Singapore and the United States, and should not be relied upon by or be passed to other persons.

The First Sentier Investors funds referenced in these materials are not registered for sale in the United States and this document is not an offer for sale of funds to US persons (as such term is used in Regulation S promulgated under the 1933 Act). Fund-specific information has been provided to illustrate First Sentier Investors’ expertise in the strategy. Differences between fund-specific constraints or fees and those of a similarly managed mandate would affect performance results.

About First Sentier Investors

References to ‘we’, ‘us’ or ‘our’ are references to First Sentier Investors, a global asset management business which is ultimately owned by Mitsubishi UFJ Financial Group (MUFG). Certain of our investment teams operate under the trading names FSSA Investment Managers, Stewart Investors and Realindex Investments, all of which are part of the First Sentier Investors group.

This material may not be copied or reproduced in whole or in part, and in any form or by any means circulated without the prior written consent of First Sentier Investors.

We communicate and conduct business through different legal entities in different locations. This material is communicated in:

Australia and New Zealand by First Sentier Investors (Australia) IM Limited, authorised and regulated in Australia by the Australian Securities and Investments Commission (AFSL 289017; ABN 89 114 194311)

European Economic Area by First Sentier Investors (Ireland) Limited, authorised and regulated in Ireland by the Central Bank of Ireland (CBI reg no. C182306; reg office 70 Sir John Rogerson’s Quay, Dublin 2, Ireland; reg company no. 629188)

Hong Kong by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities & Futures Commission in Hong Kong. First Sentier Investors and FSSA Investment Managers are business names of First Sentier Investors (Hong Kong) Limited.

Singapore by First Sentier Investors (Singapore) (reg company no. 196900420D) and this publication or advertisement has not been reviewed by the Monetary Authority of Singapore. First Sentier Investors (registration number 53236800B) and FSSA Investment Managers (registration number 53314080C) are business divisions of First Sentier Investors (Singapore).

Japan by First Sentier Investors (Japan) Limited, authorised and regulated by the Financial Service Agency (Director of Kanto Local Finance Bureau (Registered Financial Institutions) No.2611)

United Kingdom by First Sentier Investors (UK) Funds Limited, authorised and regulated by the Financial Conduct Authority (reg. no. 2294743; reg office Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB)

United States by First Sentier Investors (US) LLC, authorised and regulated by the Securities Exchange Commission (RIA 801-93167).

To the extent permitted by law, MUFG and its subsidiaries are not liable for any loss or damage as a result of reliance on any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment products referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

© First Sentier Investors Group