This is a financial promotion for FSSA Global Emerging Markets Strategies. This information is for professional clients only in the UK and elsewhere where lawful. Investing involves certain risks including:

- The value of investments and any income from them may go down as well as up and are not guaranteed. Investors may get back significantly less than the original amount invested.

- Currency risk: the Fund invests in assets which are denominated in other currencies; changes in exchange rates will affect the value of the Fund and could create losses. Currency control decisions made by governments could affect the value of the Fund's investments and could cause the Fund to defer or suspend redemptions of its shares.

- Emerging market risk: Emerging markets tend to be more sensitive to economic and political conditions than developed markets. Other factors include greater liquidity risk, restrictions on investment or transfer of assets, failed/delayed settlement and difficulties valuing securities. .

For details of the firms issuing this information and any funds referred to, please see Terms and Conditions and Important Information.

For a full description of the terms of investment and the risks please see the Prospectus and Key Investor Information Document for each Fund.

If you are in any doubt as to the suitability of our funds for your investment needs, please seek investment advice.

FSSA GEM Focus strategy reaches 5-year anniversary

Quarterly Manager Views - December 2022

Investment management is an industry where in the short run there is usually little relationship between process and outcome. In the long run, however, the link is very strong. Five years ago we launched the FSSA Global Emerging Markets Focus strategy. It has been an interesting time to invest in emerging markets — we have witnessed the tragic war unfold in Ukraine, increased geopolitical tensions between the US and China, panic over the election of leftist governments in Latin America, nationwide lockdowns in response to Covid-19 and a brief period during 2020/2021 where we began to question the sanity of markets (refer to our note on Growth Traps). Over this period, we have stuck to our long-established investment process, which emphasises bottom-up, benchmark-agnostic portfolio construction, with particular focus on the quality of management, the quality of franchise and, last but not least, valuation discipline.

We tend not to comment on performance in these letters, but as five years have now passed we think it an appropriate point to pause and take stock of the journey so far. A patient investor in our fund would have received an annualised return of 5.2%1 (in AUD, net of fees) compounded over these five years. This is a touch disappointing and below what we expected when we set out five years ago. To be sure, it is more than the return from the benchmark index (MSCI Emerging Markets) which has returned 2.1% annualised through the same period. However, whilst we struggle to be satisfied by the absolute returns, we are encouraged by the underlying operational performance of our key holdings during this tough period.

We are constantly trying to learn and improve our investment process. Naturally then, we felt it pertinent to reflect on the past five years and share our learnings.

“Time in” the market is more important than “timing” the market

This old adage, often quoted by Warren Buffet, has certainly been true for our strategy. It is rare to identify companies that have both a quality management team and a franchise that compounds free cash flows (or book value per share) at attractive rates for long periods of time. Where we have managed to find such companies, we believe the most important thing is to hold on and do nothing. Of the Top 10 contributors to fund performance over the past five years, six are companies we have owned throughout the period and three have been in the portfolio for around three years. MercadoLibre is a case in point — we have owned the company since inception of the strategy. As Latin America’s leading e-commerce company, sales have grown nearly eight-fold over the past five years. However, given the fact that poorly-run e-commerce businesses can destroy value at breathtaking scale, we are firmly focused on the cash flows. In this regard too, the results have been impressive: free cash flow (FCF) has grown five-fold, from USD200m in 2017 to an estimated USD1bn in 2022. This has driven the 28% CAGR2 total shareholder return over this period. In 2021, when we noticed that valuations had swung to an extreme (10x Enterprise Value-to-Sales!), we decided to take some profit off the table, which proved to be prudent as the share price then fell 70% from the peak. We have since bought back at lower prices and reinstated our previous position size.

Owning a quality company through a period of turbulence is a test of patience and conviction. For example, HDFC Bank, which has been a team favourite for nearly 20 years, has been undergoing a period of readjustment following the retirement of its founder CEO, Aditya Puri, after a successful 26-year stint. Over the past five years, the bank has compounded book value per share (BVPS) at its usual (stellar) pace of 20% CAGR, but valuations have de-rated owing to some short-term concerns. As a result, total shareholder return has been just 12% CAGR, which, whilst good enough on an absolute basis, should improve over the coming five years. Capitec, one of the leading banks in South Africa, is another example of a compounding machine. Despite the macroeconomic challenges in the country (more on that topic later), the bank has delivered 12% CAGR total shareholder returns over the past five years in USD terms. This has been driven by the highly profitable lending operation combined with a low-cost deposit base (the bank consistently earns an astonishing 5% return on assets). As a result, BVPS has grown at 17.5% CAGR over five years, underpinning shareholder returns.

For good quality companies, time becomes your friend. We will endeavour to find these kind of companies and hold them as long as possible.

Overwhelmed by macro

Our team has a long track record of investing in what many would deem to be difficult markets. In general, we have focused on finding companies that are able to withstand (perhaps even thrive) in volatile macroeconomic environments. However, in some rare instances, external macroeconomic issues can completely swamp even the best-run company. In this regard, it is worth recounting our investment in the Argentine bank Grupo Financiero Galicia. During 2017, our meetings with the CEO and several other members of the senior management team pointed to a culture that we liked and a franchise that was inherently strong — the bank had averaged 37% return on equity (ROE) for the previous 5-year period. More importantly, its performance was underpinned by a good deposits franchise (11% of all private deposits in the country). With the country electing a new leader, President Mauricio Macri, it seemed as if Argentina would regain its former glory and the issue of hyperinflation would finally be controlled. However, shortly after we made our investment, politics in the country took a dramatic U-turn (left turn?) and the economy, which had been improving, was destabilised yet again. Despite the bank performing well operationally, the intense currency headwind meant that we subsequently sold out of our position at a loss. This has been our single largest detractor since inception, costing us close to 250 bps of performance.

Another example of a mistake where we underestimated the macroeconomic headwinds was the case of AVI Limited, a leading consumer staples company in South Africa. In this instance, we were mainly attracted by the returns-focused CEO and his approach to capital allocation. The company had generated 25% returns on capital employed (ROCE) for the 10-year period prior to our investment and managed to deliver 25% during the 2017-22 period as well. However, the company was unable to grow faster than the currency was depreciating, leading to flat revenues and profit for over five years. It turned out to be what we refer to as a “weak compounder”. This lack of growth meant that valuations were steadily de-rated and we eventually sold our position to fund better ideas elsewhere.

These have been expensive lessons, with the outcome being that we now systematically check and limit our portfolio exposure to so-called “high-risk” economies (simplistically defined as those with adverse macroeconomic conditions).

Stay disciplined

One area that is perhaps overlooked when it comes to investment performance are the mistakes that were avoided. During late 2020 and through 2021, we witnessed a global market mania that perhaps hadn’t been seen for decades. There was a frenzy of initial public offerings (IPOs), most of which had dubious business models and sketchy financials. Meanwhile, valuations lost all relation with fundamentals as companies that were beneficiaries of Covid-induced work-from-home strictures were bid up to stratospheric levels. Most of the “stars” of this time were businesses that we call “Growth Traps”. They are characterised by a business model wherein a constant supply of capital is needed to fund operating losses, as the profit pool of an established industry (such as advertising or retail) is transferred to customers. There is no evidence yet of such companies being able to capture the profit pool they have destroyed in their quest for scale.

In these phases, it is important to stay disciplined and not be enticed into overpaying for stocks. Our team helps us stay grounded and avoid mistakes in times like these. We have not participated in any IPOs for the GEM strategy over the past few years, most of which are now languishing below the listing price. Nor have we bought into flawed business models that promise a “path to profitability”.

Conviction comes from thinking long term

The Covid-19 pandemic has dominated most aspects of life and business for nearly three years now, with places like China still battling the spread of the virus. Several of our holdings were also significantly challenged during the pandemic as the unprecedented lockdowns took its toll on their businesses.

For instance, the Mexican Starbucks operator, Alsea, had never experienced same-store sales declines of more than 4% prior to the pandemic, but during the second quarter of 2020, sales declined by 60-70%! For some of our travel-related companies, like Mexican airport operator Grupo ASUR, or the leading Online Travel Agent (OTA) in Latin America Despegar, the year-on-year sales decline was even greater, at 95%. The financial services companies we owned, such as Indian private-sector banks HDFC Bank or ICICI Bank, were also dealing with unprecedented circumstances whereby they didn’t know if a majority of their borrowers would be able to make interest payments, given the national lockdown imposed in India during April-May 2020.

At this point, we took a step back and conducted a deep-dive review of our holdings. We had calls with management teams and re-evaluated their businesses. Fortunately, this gave us greater conviction in the longer-term trajectory of our holdings. The majority of them are market leaders in their respective industries and we realised that if they were struggling, their competitors would be even worse off. From our conversations, it became increasingly clear that when the lockdowns eventually ended, our holdings should have even higher market share and face less competition. Not only that, but because they were cutting costs (by renegotiating rental agreements and supplier contracts, and focusing on efficiency), operational leverage should result in an expansion of margins, which in many cases would outstrip their pre-pandemic highs. As such, even though the early stages of the pandemic were particularly challenging, we tried to look beyond the immediate situation — and we found some very attractive bargains, especially among Indian private-sector banks and Latin American restaurant and travel companies.

Overall, this period of volatility has kept us on our feet and truly tested our conviction in the long-term potential of the businesses we owned. We are now quietly hopeful that the next period will be quite rewarding for the strategy.

Stick to the process

As we look forward, we couldn’t be more pleased with our team and the investment process that we have in place. Our emphasis remains on preserving capital and growing it sustainably, simple though it sounds. Over the more-than-30 years since the establishment of the FSSA team, the investment process has been honed continually, taking these and other painful lessons along the way to evolve the process accordingly. While the next five years are unlikely to look like the previous five, we will continue to work hard on delivering satisfactory returns to our clients.

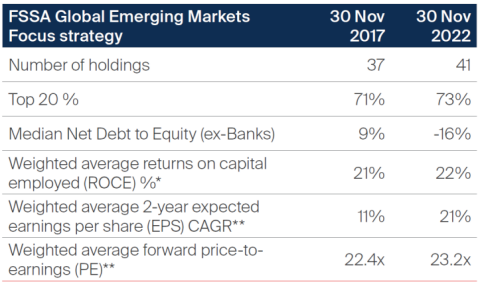

Over the past five years, the strategy has been consistent in terms of the number of holdings and concentration of the portfolio. The quality of the franchises we own has also been steady, reflected in the ROCE they generate. As we come out of the pandemic and economies recover, especially in places like China and India, we expect increased prospects for growth. This shows up in the consensus estimates for the earnings of our set of holdings.

Source: FSSA Investment Managers, Bloomberg. *Return on equity (ROE) for GICS Financial companies, and Pre-tax ROCE (i.e. earnings before interest and taxation (EBIT)/Capital Employed) for other portfolio companies. ** Based on Bloomberg consensus estimates.

Overall, this makes us very optimistic about the future of the FSSA GEM Focus strategy and we believe that the best is still yet to come!

In this letter, we have tried to cover points which we think might be of interest to the strategy’s investors. If there are any questions or feedback concerning the strategy, our approach or operations, we would welcome hearing from you.

Thank you for your support.

1 For the FSSA Global Emerging Markets Focus Fund AUT, as at 30 November 2022

2 Compound annual growth rate

Investment insights

- Article

- 5 mins

- Article

- 10 mins

- Article

- 6 mins

Source: Company data retrieved from company annual reports or other such investor reports. Financial metrics and valuations are from FactSet and Bloomberg. As at 30 November 2022 or otherwise noted.

Important Information

This material has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (FSI AIM, FSSA Investment Managers). The FSSA Investment Managers business forms part of First Sentier Investors, which is a global asset management business that is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group. A copy of the Financial Services Guide for FSI AIM is available from First Sentier Investors on its website.

This material is directed at persons who are ‘wholesale clients’ (as defined under the Corporations Act 2001 (Cth) (Corporations Act)) and has not been prepared for and is not intended for persons who are ‘retail clients’ (as defined under the Corporations Act). This material contains general information only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. The product disclosure statement

(PDS) or Information Memorandum (IM) (as applicable) for the FSSA Global Emerging Markets Focus Fund (ARSN: 610 729 005)

(Fund), issued by The Trust Company (RE Services) Limited (ABN 45 003 278 831, AFSL 235150) (Perpetual)], should be considered before deciding whether to acquire or hold units in the Fund(s). The PDS or IM are available from First Sentier Investors.MUFG, FSSA Investment Managers, their respective affiliates and any service provider to the Fund do not guarantee the performance of the Fund or the repayment of capital by the Fund. Investments in the Fund are not deposits or other liabilities of MUFG, FSSA Investment Managers, their respective affiliates or any service providers to the Fund and investment-type products are subject to investment risk including loss of income and capital invested.

Any opinions expressed in this material are the opinions of the individual author at the time of publication only and are subject to change without notice. Such opinions: (i) are not a recommendation to hold, purchase or sell a particular financial product; (ii) may not include all of the information needed to make an investment decision in relation to such a financial product; and (iii) may substantially differ from other individual authors within First Sentier Investors.

To the extent permitted by law, no liability is accepted by MUFG, FSSA Investment Managers nor their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that FSSAM Investment Managers believes to be accurate and reliable, however neither MUFG, FSSA Investment Managers nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of FSSA Investment Managers.

Any performance information has been calculated using exit prices after taking into account all ongoing fees and assuming reinvestment of distributions. No allowance has been made for taxation. Past performance is not indicative of future performance.

Copyright © First Sentier Investors, 2023