Please read the following important information for FSSA Indian Subcontinent Fund

• The Fund invests primarily in equity securities and equity related securities in Indian subcontinent which may expose to potential changes in tax, political, social and economic environment.

• The Fund invests in emerging markets which may have increased risks than developed markets including liquidity risk, currency risk/control, political and economic uncertainties, high degree of volatility, settlement risk and custody risk.

• Investing in small /mid-capitalisation securities may have lower liquidity and their prices are more volatile to adverse economic developments.

• The Fund’s investments may be concentrated in a single country/ sector, specific region or small numbers of countries/ companies which may have higher volatility or greater loss of capital than more diversified portfolios.

• The Fund may use FDIs for hedging and efficient portfolio management purposes, which may subject the Fund to additional liquidity, valuation, counterparty and over the counter transaction risks.

• It is possible that a part or entire value of your investment could be lost. You should not base your investment decision solely on this document. Please read the offering document including risk factors for details.

FSSA Indian Subcontinent Fund

Monthly Manager Views - April 2021

As bottom-up investors, the FSSA team carry out well over 1,500 meetings each year to assess company managements’ capabilities and the underlying strength of the franchises they run. These Monthly Manager Views are based on the team’s discussions with company management and the in-depth analysis that follows.

Initial Public Offerings (IPOs)

In the first three months of this year, 17 new companies have listed on the mainboard exchanges in India, more than in all of 2019 or 2020*. High levels of retail investor participation and continuing inflows for domestic mutual funds have meant that these new issuances have been lapped up by eager investors. It is not unusual for an IPO to be subscribed 100 times of its offer size or deliver substantial gains on the listing day itself. Blogs track the fluctuating “grey market premium” weeks in advance, indicating likely listing gains. For many investors, receiving an allocation for the next hot deal often takes precedence over analysis of the business itself.

Our approach towards new listings is cautious, given our focus on capital preservation. Our research process on any company begins by assessing our alignment with the majority owners and senior management. In particular, we observe how the owners behaved during difficult periods for the business — whether they have compromised the interests of minority shareholders or any other stakeholders to extract more value for themselves. We also like to view business performance across cycles, to learn about its pricing power and competitive position. Such track record of management’s actions and business performance over long periods is not available in the case of new listings. We have thus been selective in our investments in IPOs. 490 companies have listed in India over the last five years*. We have participated in just nine of these transactions.

HDFC Standard Life Insurance Company and Metropolis Healthcare are two such examples. We had been shareholders of HDFC Standard Life’s parent Housing Development Finance Corporation, as well as HDFC Bank, for several years when it listed in 2017. In our experience, the Group’s governance standards are among the highest across our investment universe. We began meeting HDFC Standard Life as early as 2004 and had met its top management on 11 occasions before its IPO. These meetings and our long association with its parent gave us the conviction to be among the anchor investors in its IPO. In the case of Metropolis Healthcare, our due diligence involved several meetings with its CEO, Ameera Shah, as well as its listed and unlisted peers. Our discussions with Vivek Gambhir, then CEO of Godrej Consumer Products and an independent director on Metropolis’ board, highlighted Ameera’s focus on setting industry benchmarks in testing quality. Customer awareness about the need for accurate diagnostic testing has increased significantly, particularly during the Covid-19 pandemic. This has led to Metropolis consistently gaining market share from smaller laboratories with poor testing standards. Our conviction in its potential to drive industry consolidation has only grown since our investment in its IPO in 2019.

The life insurance and diagnostics industries are among the various sectors which are relatively new to the listed universe in India. Scalable and profitable businesses in industries such as gaming, e-commerce, on-demand local services (food delivery and others) and online education have emerged in other large global markets. Companies in these industries have largely been privately funded in India until now. As these businesses are likely to list on public markets in the coming periods, India’s investment universe has the potential to change significantly. We are following this change closely, by meeting the management teams of several unlisted businesses across industries. These meetings help us assess the development of these businesses as well as the competitive implications for our existing portfolio companies.

Our cautious approach towards investing in new listings has held us in good stead. 254 of the 490 companies (52% of total) which have listed in India over the last five years have delivered negative total returns since listing. Median returns across all IPOs during this period is -3%. In contrast, seven of our nine investments in new listings over this period have been profitable, with a median gain of 52%*. We are excited about the potential of new companies from fast-growing industries being listed in India. But we will stick to our cautious approach, focused on preserving our clients’ capital.

Performance Commentary for April 2021

The fund’s performance in April was weak. The key detractors were Mahindra Lifespace Developers, HDFC Bank and Blue Star Limited. These companies are among the fund’s top ten holdings, and our conviction in each remains high.

The decline in the share prices of Mahindra Lifespace Developers and Blue Star was linked to concerns about the impact of the second wave of the Covid-19 pandemic on customer demand for their real estate and air-conditioner businesses respectively. While movement restrictions are likely to affect demand over the short term, both companies have strong balance sheets and witnessed a rapid improvement in customer demand when lockdown restrictions were previously eased. We expect a similar outcome in the coming period as well. Given their leading industry positions, we believe both companies are likely to gain market share from smaller competitors which are struggling in this period.

HDFC Bank’s share price performance was affected by recurring issues with its technology infrastructure. The bank has witnessed five system outages since 2019. Following our recent discussion with its CEO and CFO, we gained comfort in their plans to invest significantly to upgrade the bank’s technology infrastructure. Their previous technology investments have allowed HDFC Bank to emerge as the leader across various digital services and channels. We are confident that its management will address the current issues successfully.

The key positive contributors during the month were ICICI Bank, Computer Age Management Services (CAMS) and Mahindra CIE Automotive.

ICICI Bank reported strong quarterly performance. Its domestic advances grew by 18% compared to the same quarter last year, its deposits grew by 21% and it reported Return on Assets (ROA) of 1.5%. The bank has maintained strong asset quality and high levels of provision coverage against potential bad loans despite the impact of Covid-19 on various segments of the economy.

Computer Age Management Services (CAMS) has benefited from strong performance in its core mutual fund transfer agency business, in which it is the dominant market leader. Its management is also launching several value-added services, which have the potential to accelerate its growth in the coming periods.

Mahindra CIE Automotive also reported strong quarterly performance across both its Indian and European operations. The company gained from a sharp rebound in customer demand which led to 32% growth in its revenues compared to the same period last year. Its cost-cutting measures have led to a significant improvement in its profitability, which led to its net profit rising by 133% compared to the same period last year.

* Source: IIFL Securities, FSSA Investment Managers. As of 15 March 2021.

Source: First Sentier Investors as at 30 April 2021. The Fund is a sub fund of Ireland domiciled First Sentier Investors Global Umbrella Fund Plc.

Cumulative Performance in USD (%)

Calendar Year Performance in USD (%)

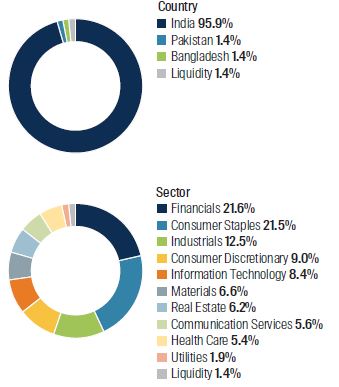

Asset allocation (%)†

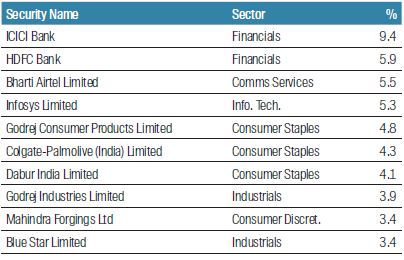

Top 10 company holdings (%)

Source: Company data, FSSA Investment Managers, as 30 April 2021 or otherwise noted.

Important Information

The Fund is a sub fund of Ireland domiciled First Sentier Investors Global Umbrella Fund Plc. * Class I (USD-Acc) is the non-dividend distributing class of the fund. The performance quoted are based on USD total return (non-dividend distributing) of the respective class.

Δ MSCI India Net Index. Gross of tax benchmark performance is shown before 1 July 2016 and net of tax benchmark performance is shown after the aforementioned date. The Fund may hold multiple equity securities in the same company, which have been combined to provide the Fund’s total position in that company. Index weights, if any, typically include only the main domestic-listed security. The above Fund weightings may or may not include reference to multiple securities. On 22 September 2020, First State Indian Subcontinent Fund was rebranded as FSSA Indian Subcontinent Fund.

† Allocation percentage is rounded to the nearest one decimal place and the total allocation percentage may not add up to 100%.

Unless otherwise specified, all information contained in this document is as at 31 March 2021. Investment involves risks, past performance is not a guide to future performance. Refer to the offering documents of the respective funds for details, including risk factors. The information contained within this document has been obtained from sources that First Sentier Investors believe to be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness, accuracy or completeness of the information. Neither First Sentier Investors, nor any of its associates, nor any director, officer or employee accepts any liability whatsoever for any loss arising directly or indirectly from any use of this. It does not constitute investment advice and should not be used as the basis of any investment decision, nor should it be treated as a recommendation for any investment. The information in this document may not be edited and/or reproduced in whole or in part without the prior consent of First Sentier Investors.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of FSSA Investment Managers’ portfolios at a certain point in time, and the holdings may change over time.

This document is issued by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong. First Sentier Investors and FSSA Investment Managers are business names of First Sentier Investors (Hong Kong) Limited. The FSSA Investment Managers logo is a trademark of the MUFG or an affiliate thereof.

First Sentier Investors (Hong Kong) Limited is part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. First Sentier Investors includes a number of entities in different jurisdictions.

MUFG and its subsidiaries are not responsible for any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.