Please read the following important information for FSSA Indian Subcontinent Fund

• The Fund invests primarily in equity securities and equity related securities in Indian subcontinent which may expose to potential changes in tax, political, social and economic environment.

• The Fund invests in emerging markets which may have increased risks than developed markets including liquidity risk, currency risk/control, political and economic uncertainties, high degree of volatility, settlement risk and custody risk.

• Investing in small /mid-capitalisation securities may have lower liquidity and their prices are more volatile to adverse economic developments.

• The Fund’s investments may be concentrated in a single country/ sector, specific region or small numbers of countries/ companies which may have higher volatility or greater loss of capital than more diversified portfolios.

• The Fund may use FDIs for hedging and efficient portfolio management purposes, which may subject the Fund to additional liquidity, valuation, counterparty and over the counter transaction risks.

• It is possible that a part or entire value of your investment could be lost. You should not base your investment decision solely on this document. Please read the offering document including risk factors for details.

FSSA Indian Subcontinent Fund

Monthly Manager Views - October 2021

Godrej Industries

Our investment philosophy is to back owners and managers with whom we feel strongly aligned. These owners typically have track records of treating all stakeholders fairly, in both good and bad times. They are ambitious in growing their business, but also risk-aware in their pursuit of growth. In India, we typically find these traits in family-owned companies (commonly referred to as “promoter groups”). Families are able to take a multi-decade view of their business and act counter-cyclically to create value for all shareholders. Our favoured promoter groups are those who recognise the advantages of introducing professionally-run management teams, high-quality boards and other best practices with respect to governance. We follow such changes closely to identify the cultural markers of families which are likely to succeed over time, and others that may be left behind.

The Godrej group was founded in 1897 and has been stewarded by the family successfully across generations. Its current leaders, Pirojsha and Nisaba Godrej, are from the fourth generation of the family. While they lead the group’s governance, the day-to-day operations of each underlying business are led by talented professional managers. This combination of family ownership and professional management has helped Godrej build leading businesses in segments ranging from Home & Personal Care products to Residential Real Estate and Animal Feed. Godrej Industries is the group’s listed holding company, which owns a 24% stake in Godrej Consumer Products, 47% in Godrej Properties and 62% in Godrej Agrovet. It has a track record of successfully incubating new businesses, such as Godrej Properties, which was listed in 2010 (current market capitalisation of USD 8.6bn) and Godrej Agrovet, which was listed in 2017 (current market capitalisation of USD 1.6bn). We have been shareholders of Godrej Industries for the most part of the last decade.

Recent developments at the company have been encouraging. Its board has been refreshed with four new independent directors as long-standing directors retired. The new board members include the ex-CFO of Novartis India, a partner associated with Fidelity International, the co-founder of a reputed Venture Capital firm and the chairman of a leading Home and Kitchenware brand. Additionally, Godrej Housing Finance, which was set up in 2020, has been injected by the family into Godrej Industries for a nominal sum, and Manish Shah, an executive with significant experience at Citigroup, was appointed its CEO. Given the strong reputation of the Godrej group, the housing finance business is able to access funding at attractive rates. Its pilot program with Godrej Properties has received a strong customer response. Similar to Godrej Properties and Godrej Agrovet, we believe this business has potential to create significant value over the long term.

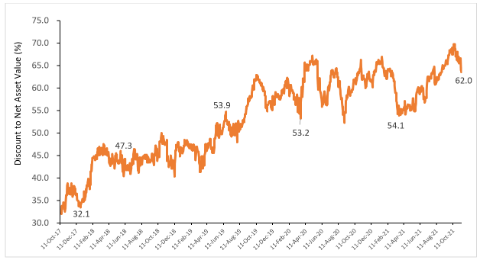

Godrej Industries’ shareholding in Godrej Consumer Products and Godrej Properties account for 90% of its net asset value. Godrej Consumer Products’ growth has been weak in recent years. It recently appointed Sudhir Sitapati, who has spent over two decades at Unilever, as its new CEO. We expect its performance to improve under Mr Sitapati’s leadership. Godrej Properties is benefiting from the consolidation in India’s fragmented real estate industry, as poor-quality local developers lose out to leading brands like Godrej. These expectations are reflected in its expensive valuations. In stark contrast, Godrej Industries’ valuations are exceptionally attractive, in our view, at a 62% discount to the value of its stakes in its listed subsidiaries and associates. The family appears to share the same view, having increased its stake in Godrej Industries by 6% since 2019.

| Market Value* (INR million) | Godrej Industries' Shareholding | Per share value for Godrej Industries (INR) | % of Net Asset Value Per Share** | |

|---|---|---|---|---|

| Godrej Consumer Products | 939854 | 23.8% | 665 | 38% |

| Godrej Properties | 637425 | 47.3% | 897 | 52% |

| Godrej Agrovet | 116555 | 62.5% | 173 | 10% |

| Standalone Net Debt | -29126 | -87 | ||

| Net Asset Value Per Share (INR) | 1648 | |||

| Current market price (INR) | 631 | |||

| Discount to Net Asset Value | 62% |

Godrej Consumer Products

- Market Value* (INR million)

- 939854

- Godrej Industries' Shareholding

- 23.8%

- Per share value for Godrej Industries (INR)

- 665

- % of Net Asset Value Per Share**

- 38%

Godrej Properties

- Market Value* (INR million)

- 637425

- Godrej Industries' Shareholding

- 47.3%

- Per share value for Godrej Industries (INR)

- 897

- % of Net Asset Value Per Share**

- 52%

Godrej Agrovet

- Market Value* (INR million)

- 116555

- Godrej Industries' Shareholding

- 62.5%

- Per share value for Godrej Industries (INR)

- 173

- % of Net Asset Value Per Share**

- 10%

Standalone Net Debt

- Market Value* (INR million)

- -29126

- Godrej Industries' Shareholding

- Per share value for Godrej Industries (INR)

- -87

- % of Net Asset Value Per Share**

Net Asset Value Per Share (INR)

- Market Value* (INR million)

- 1648

Current market price (INR)

- Market Value* (INR million)

- 631

Discount to Net Asset Value

- Market Value* (INR million)

- 62%

*Market value of Godrej Consumer Products, Godrej Properties and Godrej Agrovet, as at 12th November 2021.

**The % of Net Asset Value is adjusted for the standalone net debt. Source: FactSet, BSE India.

Godrej Industries’ Discount to Net Asset Value since the listing of Godrej Agrovet

Source: ICICI Securities, 12th November 2021

Performance Commentary

The FSSA Indian Subcontinent Fund declined in October. The key contributors to performance were ICICI Bank and Mahindra CIE Automotive.

ICICI Bank rose after it reported strong quarterly results. Its Net Interest Income (NII) rose by 25% and earnings per share (EPS) by 29% over the same period last year. The bank’s asset quality and Return on Assets (ROA) continue to improve steadily.

Mahindra CIE Automotive also rose after it reported strong financial performance. Its revenues grew by 21% and operating profit by 78% over the same period last year. The company benefited from a rebound in automotive demand in both its Indian and European operations, and market share gains. Its efforts to improve operating efficiency over the last year has helped it strengthen its profitability.

The key detractors were Solara Active Pharma and Colgate Palmolive (India).

Solara Active Pharma declined due to concerns about price inflation on its key raw materials. However, our discussions with the management reassured us that the long-term prospects are still bright, with the CEO stating an ambition to grow revenues nearly four-fold over the coming five years.

Colgate Palmolive (India) declined following concerns about rising commodity costs affecting its profitability. It has dominant market share in oral care which affords the company strong pricing power. Colgate has a long track record of improving its profitability consistently. In our view, it will be able to continue improving its profitability over the medium term, as it passes on price increases to consumers and upgrades its product portfolio to more premium products.

*Company data retrieved from company annual reports or other such investor reports. Financial metrics and valuations are from FactSet and Bloomberg. As at 31 October 2021 or otherwise noted.

Important Information

Investment involves risks, past performance is not a guide to future performance. Refer to the offering documents of the respective funds for details, including risk factors. The information contained within this document has been obtained from sources that First Sentier Investors (“FSI”) believes to be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness, accuracy or completeness of the information. Neither FSI, nor any of its associates, nor any director, officer or employee accepts any liability whatsoever for any loss arising directly or indirectly from any use of this. It does not constitute investment advice and should not be used as the basis of any investment decision, nor should it be treated as a recommendation for any investment. The information in this document may not be edited and/or reproduced in whole or in part without the prior consent of FSI.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of FSSA Investment Managers’ portfolios at a certain point in time, and the holdings may change over time.

This document is issued by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong. First Sentier Investors is a business name of First Sentier Investors (Hong Kong) Limited.

First Sentier Investors (Hong Kong) Limited is part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. First Sentier Investors includes a number of entities in different jurisdictions..

MUFG and its subsidiaries are not responsible for any statement or information contained in this document. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.