Climate change

Team climate change statement

At FSSA, we have always believed that looking at sustainability challenges and opportunities are a core part of investment decision-making and can have a large impact on how a company makes money. We actively seek to invest in businesses whose sustainable practices and products are able to meet the world’s changing expectations.

This matters to us because as long-term investors, we expect that companies will have to bear the costs of meeting these challenges over the course of our ownership.

Many of the countries we invest in are particularly vulnerable to climate-related risks given their geography and economy. Therefore, we expect that every company we invest in will be exposed to some form of climate risk. Specifically, we invest large amounts in financial services and companies supplying basic essential items known as consumer staples. To assess climate risk in the finance sector, we focus on lending practices and the impact this has on climate change. For consumer staples, the most significant environmental topics are raw material use, water management and plastics pollution.

Climate risks – including those related to the transition to low-carbon economies (transition risks), the physical impacts of climate change (physical risks), reputational concerns, and regulatory and legal requirements – are all interconnected issues. Of these, we consider the biggest risks to our investments, and those that we can address directly with companies, to be transition risks and physical risks.

Transition risks are growing in consideration for investors as companies think through the societal and economic shifts which are necessary to move towards a low-carbon future. We see them as immediate challenges for companies to address. Whilst our direct exposure to fossil fuels, agriculture and mining is minimal, these businesses form a meaningful part of our investee companies’ supply chains. We therefore consider these risks from an industry perspective as well as from a company-by-company point of view.

Physical risks refer to the impacts of a changing and volatile climate on existing business practices. As such, we believe this affects all companies – either through their usual business activities or their supply chains and sales activities.

Beyond these two primary risks, companies also face more stringent regulatory and legal risks, which increases the risk of reputational damage. The governments of countries in which we invest have begun to implement penalties for non-compliance. We fully expect these risks to increase over time.

We identify climate-related risks throughout the research process, from the initial company assessment to the ongoing monitoring and review process. We believe the most effective way to identify risks is through regular engagement and meetings with a company’s management. This also provides us with an opportunity to assess other factors and determine whether a company’s efforts to manage climate risks are genuine.

To evaluate a company’s climate-related risks and opportunities and to prepare for these conversations with management, we review company disclosures and data from third-party providers such as Institutional Shareholder Services (ISS) and Morgan Stanley Capital International (MSCI) to provide us with a company’s historical carbon intensity and scope 11 and scope 22 emissions. Additionally, we use Sustainalytics and RepRisk, among others, to alert us of significant recent events and controversies. We use these findings to augment our engagement with companies.

Throughout the engagement process, we identify areas where companies could improve and offer external resources that may assist in the process. For example, we encourage companies to utilise established frameworks like Task Force on Climate-related Financial Disclosures (TCFD) and the Science-Based Targets initiative (SBTi) to report on their climate-related disclosure and targets.

At this stage, we do not conduct separate scenario analyses as it relies heavily on unknowable assumptions, particularly around what are called scope 3 emissions3.

1 Scope 1 emissions are direct GHG emissions occur from sources that are owned or controlled by the company, for example, emissions from combustion in owned or controlled boilers, furnaces, vehicles, etc.

2 Scope 2 emissions accounts for GHG emissions from the generation of purchased electricity consumed by the company. Purchased electricity is defined as electricity that is purchased or otherwise brought into the organizational boundary of the company.

3 Scope 3 emissions is an optional reporting category that allows for the treatment of all other indirect emissions. Scope 3 emissions are a consequence of the activities and operation of the reporting company within its value chain.

We manage climate-related risks by looking at the companies in our portfolios individually and collectively.

We conduct fund-level sustainability reviews with environmental and social indicators to identify the companies which are significantly above or below the average, which then focuses our engagement efforts. Specific to climate risks, we review total carbon emissions, trends in emissions intensity, quality of disclosure and alignment to SBTi. We launched a decarbonisation review process in 2021 with an assessment of how the companies that we invest in were tackling their carbon footprint reductions. This included an evaluation of how they performed at that point in time and their plans for the future. With our engagement-led process, we started with an assessment of our largest positions, with the aim of driving multi-year carbon emissions reductions. We prioritised the lowest performing companies in our initial review for more pressing engagement.

In our approach, we integrate climate-related considerations throughout the research process. With every potential investment, we consider the business model and its exposure to climate-related risks, and decide whether we are comfortable with the level of risk the company faces. Assessing the quality of management is a critical component of our investment process. We look for signs that there is a long-term owner/manager who is passionate about climate issues – or is incentivised to care about this multi-decade challenge.

We may further express our views through votes on company proposals. Whilst we subscribe to proxy voting services such as Glass Lewis and Ownership Matters as a guide, the ultimate decision on how we cast our proxy votes lies with the respective investment analyst.

Our funds tend to have significantly lower carbon intensity than their respective benchmarks. However, we believe this data is best viewed as an output of our investment approach, which is centred on assessing the quality of companies holistically rather than selecting only those that perform well on this metric. We are hopeful that as the broader corporate world decarbonises, the gap between the benchmark and our portfolios will gradually close – and improve together.

We focus our efforts on reducing the total carbon emissions of the companies that we invest in. Rather than selling our carbon-intensive assets or buying companies that rely on an abundance of carbon offsets (a way of compensating for emissions of greenhouse gases (GHG)), we seek to encourage an aggressive reduction in GHG emissions among our investee companies, as is necessary to contribute to a real world reduction. We place less emphasis on grand-gesture statements and more on action and evidence.

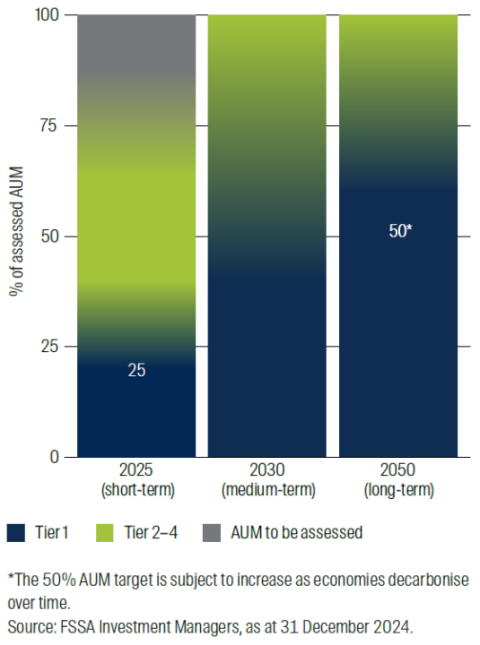

We launched our decarbonisation process in 2021 with an assessment of how the companies that we invest in were positioned, how they performed at that point in time, and their plans for the future. While we plan to engage with all of the companies on this topic, we started with the largest investments in regional and country portfolios and those in carbon-intensive sectors, covering 75% of FSSA’s total assets under management (AUM).

Our assessment is based heavily on the “net zero alignment maturity scale” from the Net Zero Investment Framework Implementation Guide (NZIFIG) produced by the Institutional Investors Group on Climate Change. We have assigned each assessed company to one of four tiers ranging from leader to laggard. The nuance in our tiers provides flexibility around a company’s direction of travel, resource constraints and purposefulness, which we think is essential in an emerging market context. (An emerging market is an economy that could experience considerable economic growth, but lacks some of the characteristics of a developed economy.)

| FSSA tier | FSSA definition | NZIF Category | Characteristics |

|---|---|---|---|

| Tier 1 Leader, track progress | A “Leader” is either achieving net zero1 with its current emissions intensity performance at, or close to, net-zero emissions; or those with adequate emissions reduction over three or more years. | “Achieving net zero” or “Aligned to a net-zero pathway” | Ambition: has set long-term goal to achieve net zero by 2050 (or earlier) Targets: announced short, medium and long-term targets Checked for alignment with the Science Based Targets initiative (SBTi) or other similar frameworks (e.g., the Transition Pathway Initiative or Climate Action 100+) Disclosure Scope 1 + 2 + material Scope 3 for three or more years2 Performance: achieved genuine reduction and/or performance relative to targets for three or more years Strategy: business model is an enabler of emissions reductions internally and externally; strategy/investment plan expected to achieve goals Capital allocation: strong capital allocation plan as part of transition plan |

| Tier 2 Committed, track progress | “Committed” means aligning to net zero, with short, medium or long-term goals (but not all), and disclosure of Scope 1 & 2 emissions data for two or more years (with an option to include material Scope 3 emissions data) | "Aligning to a net zero pathway" | Ambition: has a net-zero target, but is set beyond 2050 (i.e., not within the science-recommended timeframe) Targets: has a mix of short, medium or long-term targets, but not all Disclosure Scope 1 + 2 for two or more years; may have begun to track material Scope 3 Performance: achieved emissions reductions for two years and has a plan to achieve targets Strategy: at least part of the business is an enabler of emissions reductions internally and externally Capital allocation: has a component on capital allocation, but very low bar |

| Tier 3 Laggard, planning | “Laggard, planning” means committed to aligning towards a net-zero pathway with the intention to set clear targets, and disclosure of Scope 1 + 2 emissions data for at least one year, but with little to no progress over time | "Committed to Aligning" | Ambition: may have declared an intention to set net-zero targets, or have language supporting net zero, but there are no time-bound ambitions and key elements are missing (e.g., no organisational support, no strategy to achieve) Targets: no clear targets have been set. May have an internal target, but it is not tied to credible guidance (i.e., targets have been set randomly) DisclosureScope 1 + 2 for a minimum of one year Performance: may have disclosure and operational metrics, but little to no progress over time Strategy: may have emissions reduction as a headwind, but opportunities to reposition or evolve the business exist Capital allocation: no capital allocation plan |

| Tier 4 Laggard, needs support | “Laggard” means not aligned; those with the intention to set targets have no defined timeframes or metrics. There is poor disclosure and thus an inability to measure progress. Their business models may be structurally challenged due to a reliance on carbon-intensive resources. | "Not aligning" | Ambition: may or may not have the intention of setting a target, but no timeframe or metrics have been defined Targets: No short, medium or long-term targets defined DisclosurePoor disclosure (minimal to none), thus an inability to measure progress Performance: history of environmental malpractice and little to no improvement Strategy:may be structurally challenged due to reliance on carbon-intensive sources Capital allocation: no capital allocation plan |

1 Net zero refers to a state in which the greenhouse gases going into the atmosphere are balanced by removal out of the atmosphere. For more information, please click here.

2 Scope 1 emissions are greenhouse gas (GHG) emissions caused directly by a company in the normal operations of its business. Scope 2 emissions are indirect GHG emissions created through a company’s use and purchase of energy, while Scope 3 emissions are indirect GHG emissions throughout a company’s value chain – from suppliers to end users. For more information on GHG emissions categories, please click here.

By 2025, we aim for 25% of assessed companies to be assigned to Tier 1, aligned to net zero by 2050. We will engage with all companies under assessment to meet 100% disclosure of Scope 1 and Scope 2 emissions by 2025 and encourage the alignment of targets to the Science Based Targets initiative (SBTi).

For companies to be considered aligned to net zero, they must disclose their emissions performance and have short-, medium- and long-term targets. We recognise that companies in our portfolios are subject to different timeframes (i.e., carbon neutrality by 2060 for China and by 2070 for India). We expect our holdings to align with the IPCC’s recommendation of limiting global warming to below 1.5° Celsius and reaching net-zero emissions by 2050.

By 2030, we aim to have increased our assessment of companies to 100% of our AUM. Through our ongoing engagement, we also aim to increase the percentage of AUM assigned to Tier 1, aligned to net zero by 2050, from the initial 25%.

Rather than penalise companies that are less advanced towards their net-zero goals, we aim to make and measure progress over the years, and move all companies towards the top tier through purposeful engagement with company management. We will encourage companies to set meaningful targets with defined plans to achieve genuine reductions in carbon emissions.

We are initially committing 50% of our AUM to be aligned to achieving net zero in 2050 (assigned to Tier 1), with an aim to increase the portion of AUM towards 100% as economies gradually decarbonise.

Disclaimer

The commitments and targets set out on this website are current as of today’s date. They have been formulated by the relevant First Sentier Investors (FSI) investment team in accordance with either internally developed proprietary frameworks or are otherwise, based on the Institutional Investors Group on Climate Change’s (IIGCC) Paris Aligned Investment Initiative framework. The commitments and targets are based on information and representations made to the relevant investment teams by portfolio companies (which may ultimately prove not be accurate), together with assumptions made by the relevant investment team in relation to future matters such as government policy implementation in ESG and other climate-related areas, enhanced future technology and the actions of portfolio companies (all of which are subject to change over time). As such, achievement of these commitments and targets set out on this website depend on the ongoing accuracy of such information and representations as well as the realisation of such future matters. FSI will report on progress made towards achieving these targets on an annual basis in its Climate Change Action Plan. The commitments and targets set out on this website are continuously reviewed by the relevant investment teams and subject to change without notice.