India Monthly Manager Views - Dec 2021

Mistakes of omission

50x P/E!1 70x P/E! 100x P/E! Valuations that were outrageous just a few years ago are commonly bandied about by most of the investment community these days. But, ask any respected business owner and they would shake their head in disbelief. The difference in perspective is critical. The entrepreneur is looking at the free cash flows the business could generate over the long term, and how long it would take to recoup his or her investment if they were to buy a business in its entirety. At 80x P/E, which is not uncommon in India these days, it would take a full 19 years to recover the purchase cost, even if the business’ underlying cash flows (or earnings) compound at 15% annually, and there is no re-investment to achieve this growth. Business owners whom we rate highly would not allocate capital to such opportunities. Yet, we have seen many listed companies in India witness a significant re-rating of valuations in recent years, on the back of which they have delivered exceptional shareholder returns. Our decision to not invest, or sell out of such businesses on valuation grounds have been our mistakes of omission. Yet, when we analyse these errors, as we always do, we believe that these decisions were in keeping with our disciplined investment process, which has withstood the test of time. We discuss a few below.

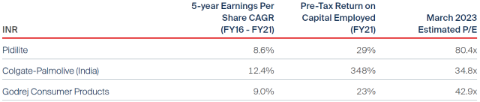

We were long-term shareholders of Pidilite until we sold our shares in 2015. The Parekh family have been excellent stewards of the business and introduced top-quality professional management, including CEO Bharat Puri, whom we had known since his days heading Cadbury India. We admired Pidilite’s ability to build and nurture strong brands that command a price premium in categories that are otherwise commoditised, such as Fevicol in adhesives. The management is also pursuing opportunities in categories like waterproofing, which can become big businesses in the coming years. With healthy Returns on Capital Employed (ROCE) (5-year average ROCE during the 2010-2015 period was 25%) and decent growth rates (sales growing at roughly 17% compound annual growth rates (CAGR) in that period), it was a core holding of ours. Given the high quality, it was not “cheap”, trading at around 22x P/E during the 2012-2014 period. Subsequently though, valuations kept rising and by 2015 they had gone past 40x P/E – a level that was higher even than fast-moving consumer goods (FMCG) peers Hindustan Unilever and Nestle India at the time! At this point, we reluctantly sold our shares, confident that we would get the chance to buy them back at more sensible valuations. Unfortunately, since then, we have seen its valuation multiple double to over 80x today. While we admire the business, its people and the opportunity ahead of it, we simply cannot fathom paying such multiples.

Instead, Colgate-Palmolive (India) and Godrej Consumer Products are today still among our largest holdings. Colgate’s brand in oral care is unrivalled. It had lost some market share in recent years, as the herbal segment grew rapidly in India. Under new CEO Ram Raghavan, it has stepped up its investments in brand building and launched innovative products, which has begun to yield results in the form of market share gains. Over the medium term, it also has the opportunity to launch other leading brands from its parent’s portfolio. Godrej Consumer Products has faced some challenges across its geographies (notably Africa) in recent years. In response, its board has appointed several strong professionals, including Sudhir Sitapati, who has spent over two decades at Unilever, as its CEO. Mr Sitapati recently laid out his plans to accelerate Godrej Consumer’s growth and improve its profitability over the medium term. We expect the company’s performance to improve under his leadership.

When we view the performance of our holdings against Pidilite, we note that Colgate has grown its earnings per share substantially faster over the last five years. It generates exceptionally high ROCE as well. Despite the challenges across Godrej Consumer’s businesses, earnings have also grown faster than at Pidilite over this period and its ROCE is only slightly lower. Yet, valuations of both Colgate-Palmolive India and Godrej Consumer are at approximately half of Pidilite’s levels (though admittedly, still high in absolute terms). Based on the strength of their franchises and the improvement we expect under their current management teams, we find the risk-reward with these companies to be much more attractive.

Source: FactSet, as at 31 December 2021

We were anchor investors in the Initial Public Offering (IPO) of Avenue Supermarts in 2017. After its valuations more than doubled after listing to over 50x forward P/E, we felt compelled to sell our holding. It is currently valued at 7x forward Enterprise Value (EV)/Sales and 115x forward P/E, compared to industry leaders such as Tesco, Sun Art and Dairy Farm which are valued below 0.5x EV/Sales and at 12x to 20x forward P/E. In fact, Avenue Supermart’s market capitalisation of USD 40bn is 35% higher than that of Tesco, while its sales are 1/23rd and profits are 1/18th of Tesco. Similarly, we find it difficult to pay 9x forward Price to Book (P/B) for India’s largest non-banking finance company valued at USD 63bn, when ICICI Bank, with a leading deposit franchise, has a market capitalisation only 20% higher and forward P/B of 3x. In some instances, our mistakes of omission have been for reasons other than valuations. We have not owned one of India’s largest conglomerates, due to our concerns around its governance practices and culture. The company is known for using its connections in the government to change policies and regulations in order to benefit itself or exert pressure on its competitors. We simply do not view this as a sustainable competitive advantage. Irrespective of how attractive its prospects or valuations become, we would not own such a business.

Fundamentally, our investment philosophy is focused on capital preservation and absolute returns and as such, we accept these mistakes of omission as an outcome of our adherence to it.

Performance commentary

The FSSA Indian Subcontinent Fund rose in December. The key contributors to performance were Infosys and Godrej Industries.

Infosys gained following the announcement of strong quarterly earnings and an upward revision of earnings guidance by one of its leading global peers. This indicated that customer demand for information technology (IT) services outsourcing remains strong.

Godrej Industries rose following an increase in the share price of Godrej Consumer Products, after its new CEO, Sudhir Sitapati announced the medium-term ambitions and strategy for the business. Its stake in Godrej Consumer Products accounts for 45% of the net asset value of Godrej Industries.

The key detractors were Solara Active Pharma and Kotak Mahindra Bank.

Solara Active Pharma declined due to concerns about inflation in prices of its key raw materials. Our discussions with the management reassured us that the long-term prospects are still bright. The management has an ambition to grow revenues nearly four-fold over the next five years.

Kotak Mahindra Bank declined due to concerns related to the emergence of a new variant of Covid-19, which could lead to disruptions in economic activity. The bank has built a strong track record of withstanding such disruptions while maintaining strong asset quality. We expect this to continue.

1 Price to earnings

*Company data retrieved from company annual reports or other such investor reports. Financial metrics and valuations are from FactSet and Bloomberg. As at 31 December 2021 or otherwise noted.

Important Information

References to “we” or “us” are references to First Sentier Investors (FSI). The FSSA Investment Managers business forms part of First Sentier Investors, which is a global asset management business that is ultimately owned by Mitsubishi UFJ Financial Group, Inc (MUFG), a global financial group.

In Hong Kong, this document is issued by First Sentier Investors (Hong Kong) Limited (FSI HK) and has not been reviewed by the Securities & Futures Commission in Hong Kong. In Singapore, this document is issued by First Sentier Investors (Singapore) (FSIS) whose company registration number is 196900420D. In Australia, this information has been prepared and issued by First Sentier Investors (Australia) IM Ltd (ABN 89 114 194 311, AFSL 289017) (FSI AIM).

This document is directed at persons who are professional, sophisticated or wholesale clients and has not been prepared for and is not intended for persons who are retail clients. The information herein is for information purposes only. It is not intended to provide you with financial product advice and does not take into account your objectives, financial situation or needs. Before making an investment decision you should consider, with a financial advisor, whether this information is appropriate in light of your investment needs, objectives and financial situation. Some of the funds mentioned herein are not authorised for offer/sale to the public in certain jurisdiction. Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of First Sentier Investors’ portfolios at a certain point in time, and the holdings may change over time.

Any opinions expressed in this material are the opinions of the individual authors at the time of publication only and are subject to change without notice. Such opinions: (i) are not a recommendation to hold, purchase or sell a particular financial product; (ii) may not include all of the information needed to make an investment decision in relation to such a financial product; and (iii) may substantially differ from other individuals within First Sentier Investors.

Please refer to the relevant offering documents in relation to any funds mentioned in this material for details, including the risk factors and information on requirements relating to investor eligibility before making a decision about investing in such funds. The offering document is available from First Sentier Investors and FSI on its website and should be considered before any investment decision in relation to any such funds.

Neither MUFG, FSI HK, FSIS, FSI AIM nor any of affiliates thereof guarantee the performance of any investment or entity referred to in this document or the repayment of capital. Any investment in funds referred to herein are not deposits or other liabilities of MUFG, FSI HK, FSIS, FSI or affiliates thereof and are subject to investment risk, including loss of income and capital invested.

To the extent permitted by law, no liability is accepted by MUFG, FSI HK, FSIS, FSI AIM nor any of their affiliates for any loss or damage as a result of any reliance on this material. This material contains, or is based upon, information that we believe to be accurate and reliable, however neither the MUFG, FSI HK, FSIS, FSI AIM nor their respective affiliates offer any warranty that it contains no factual errors. No part of this material may be reproduced or transmitted in any form or by any means without the prior written consent of FSI.

Any performance information has been calculated using exit prices after taking into account all ongoing fees and assuming reinvestment of distributions. No allowance has been made for taxation. Past performance is not indicative of future performance.

Copyright © First Sentier Investors (Australia) Services Pty Limited 2021

All rights reserved.